Although 2023 was disappointing, Chargeurs’ top-line and underlying operating profit were broadly in line with our expectations. As had been warned, the pain came from the cash flow spinner, Chargeurs Advanced Materials, in the face of order volatility. The bright side was Chargeurs Museum Studio with astounding deliveries. 2023’s low Ebit-FCF had to contend with soaring interest costs of €29.7m and gearing concerns. This need not be structural and will not derail the management’s long-term ambitions.

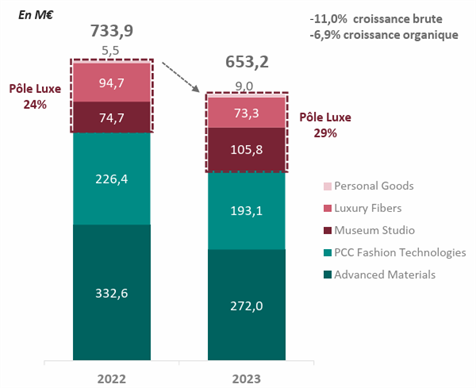

Chargeurs faced a particularly challenging 2023 environment marked by China’s slowdown, record high energy costs, high interest rates and slowing industrial sectors. Chargeurs’ FY 2023 results were penalized by the decline of Chargeurs Advanced Materials (CAM), with a negative volume effect, in spite of the Q4 23 rebound. Nevertheless, the Group’s top-line and margin figures were broadly in line with our estimates. Over 2023, Chargeurs recorded an 11% drop in revenues (of which 7% organic) to €653.2m (vs. €733.9m in 2022 and €669m expected) and an 11% drop in underlying operating profit to €26.6m (vs. €46.1m in 2022 and €26.2m expected).

Takeover bid: take up or shut up

After a particularly tumultuous 2023, Chargeurs launched its takeover bid at a price of €12, initiated by Colombus Holding and Colombus Holding 2, controlled by CEO Michaël Fribourg, with no intention of delisting its shares. Family money (Columbus and its backers) is keen to take a long-term view for Chargeurs that will not be impressed by short-term profitability swings. Effectively Columbus is offering an opportunity for short-term holders to exit gracefully. The “new” Chargeurs will be on display in Q1-2025 once the strategic plans are finalized. We would speculate that the banks – which are essential to this long-term deployment- are happy to back Columbus with limited strings attached.

Divisional revenue breakdown

On the revenue side, the performance of the Luxury and Technology divisions was very mixed in 2023, with organic growth of +3.4% and -10.1% respectively. In the technology division, Chargeurs Advanced Materials (CAM) and Chargeurs PCC Fashion Technologies (PCC-FT) both had a difficult year, with declines of 18.2% and 12.2% respectively. In H1-23, CAM was penalized by a contraction in volumes in a context of post-Covid destocking and the gradual recovery in volumes seen in Q3-23 failed to offset the fall in polyethylene costs passed through to clients. Looking ahead, Chargeurs expects volumes to improve from 2024 onwards, albeit without returning to their record levels of 2021-2022. CFT PCC, for its part, was penalized by hyperinflation and the sharp devaluation (50%) in the Argentine peso, but maintained its organic growth at 3.5% in 2023.

The Luxury division maintained its momentum, boosted by the expansion of Chargeurs Museum Studio, which reported remarkable organic sales growth of 33.5% in 2023 to €105.8m, and €120m including Hypsos. The Group reaffirmed its guidance for sales of €150m in 2024, notwithstanding the disposal of Hypsos. The Chargeurs Luxury Fibers division recorded an organic decline of 21%, with sales of €73.3m due, in particular, to the cyclone that hit its business at the beginning of the year.

Lower profitability, again penalized by CAM

On the profitability front, in line with the negative developments at CAM, Ebit fell sharply to €26.6m from €46.1m in 2023, although in line with our expectations (estimated at €26.2m). As such, CAM recorded an abnormally low level of operating income from activities, at €10.1m or 3.7% of sales, due to lower absorption of fixed costs. On the other hand, consistent with its 42% revenue growth, CMS recorded a 44% increase in its operating profit to €8.5m, bringing the margin up to 8% in 2023. CLF and CFT-PCC margins were in line with our expectations. For CFT-PCC, profitability was impacted by higher energy costs and hyperinflation, which had a €3m negative effect on EBIT, reducing the margin to 7%. As for CLF, profitability increased to 3%, against an EBIT margin of 2.1% in 2022, under cover of the NATIVA boom.

Low FCF generation putting pressure on the balance sheet

On the back of the lower EBITDA contribution (particularly at CAM), the net cash flow from operating activities fell sharply from -€7.4m to -€15.2m. Together with higher capex, the Group’s net debt position deteriorated to €235.6m at the end of 2023 from €174.7m at the end of 2022, increasing the Net Debt/EBITDA ratio to 5x from 2.6x in 2022.

The rise in interest rates, coupled with the hyperinflationary situation in Argentina, led to a sharp increase in financial expenses to €29.7m from €18.9m last year and €20.5m expected.

2024 is shaping up to be better

The worst seems to be over with signs of a rebound, notably with a recovery in volumes in the main business, CAM, which recorded 5% yoy volume growth in the Q4-23. As a result, the Group expects to generate positive operating cash flow and return to a normal level of net income. As a result Chargeurs hopes to achieve a net debt/EBITDA ratio of around 2.5-3.5x.

2025 will set the new roadmap

As Chargeurs has said, 2024 is a transitional year, even if CAM should begin to bounce back. It will take until 2025 for us to see any change at Chargeurs, when a new operating plan for the 2025-2030 cycle will be unveiled. Until then, investors will need to be patient.

The 2023 earnings release is also a turning point to some sort of a Chargeurs Mark II under the aegis of its CEO and controlling shareholder. CEO Fribourg is bent on deploying value expansion for Chargeurs as a holding company over the long run. The message is that minorities are welcomed but should not bother complaining to the management about any short-term earnings vagaries. AlphaValue will most probably revert to its analysis of Chargeurs as a HoldCo (building up asset value) as opposed to an integrated conglomerate (focused on short-term earnings and pay-outs). The target price is unlikely to suffer.