The 2019 performance was solid from a cash-generation perspective in spite of a volatile trading environment for the Protective Films division. The management’s well-placed focus in developing a diversified profit base was put in evidence as the Fashion Technologies and Museum Solutions divisions drove the group’s operating profit. After a peak investment year in the business transformation plan, Chargeurs now expects to reap the rewards come 2020 and beyond.

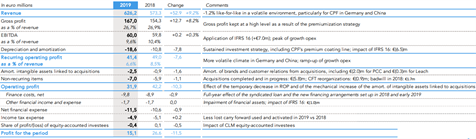

Chargeurs released full-year 2019 earnings that came slightly below our estimates at the recurring operating profit line (€41.4m), as the Protective Films division was affected by a less favourable geographic mix and a demand crunch in the key markets China and Germany. Nonetheless, the trading performance at the two other growth pillars (Fashion Technologies and Museum Solutions) supported the group’s earnings, bringing to the fore management’s strategic focus on developing a diversified profit base.

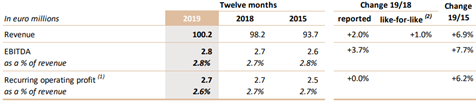

The descriptive P&L given by the company in the table below paints a clear picture of the moving parts behind the FY19 earnings.

While operational profitability did not reach the FY18 record level, cash generation from operations was fired up, coming above our expectations at €38.7m. Net cash also stood significantly above that of 2018 (€25.5m vs. €14.4m), as working capital was diligently cut through a successful group-wide action plan.

Regarding the balance sheet, the group’s net debt position increased to €122.4m as the transformative ‘Game Changers’ plan attained a peak investment year, after which Chargeurs expects to reap the returns in 2020 and beyond. The solid cash generation and current balance sheet allows the company to propose a dividend of €0.40 per share for 2019, in line with its strategy.

The challenging market conditions that characterised 2019 came as a proper test to the suitability of management’s aim to reinvent the group’s businesses and secure growth through strategic bolt-on acquisitions. So far, it appears the approach has worked. Chargeurs’ most recent undertaking saw it jazzing up a seemingly conventional business (Technical Substrates) into the group’s third growth engine, targeting an unconventional niche with strong potential (servicing museums). The newly-named Museum Solutions division is now heading towards reaching a turnover of €100m in 2020.

Tamed impact from the COVID-19 crisis, but management remains prudent

This diversification will become ever more important as the COVID-19 outbreak continues to unfold, bringing further uncertainty and volatility to markets, and impacting the demand for Chargeurs’ products and services. The company clearly addressed the subject in its earnings release, stating that, at the current stage, there has been a limited impact on its activity with no disruptions in supplies and production facilities outside China all running as usual.

Regarding the conditions in China, management cites an ‘activity rate’ above 80% of normal levels. It is of course too early to tell the full impact of the COVID-19 crisis, and management remains prudent regarding its outlook for the full year.

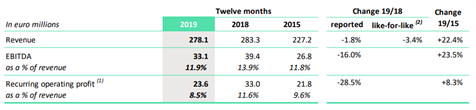

Protective Films: additional high-tech production capacity to rekindle growth

Chargeurs’ perennial moneymaker experienced a challenging 2019. While the impact from the Sino-American trade war dissipated in the second half. The impact on demand in China during H1 and in Germany throughout the entire year weighed on the division’s profitability. As the product mix in these countries is quite profitable relative to the other markets, the less favourable geographic mix was one of the reasons behind the crunch on operating margins in FY19.

The second reason was the increased costs related to the launch and ramp-up of a new sophisticated production line in Italy. The new facility will expand its current global production capacity by an impressive 20%, which seems justified by a promising order backlog for 2020. It also goes in hand with improving the product offering and moving up-market, in line with the motto that has shaped the business transformation as part of the Game Changers plan.

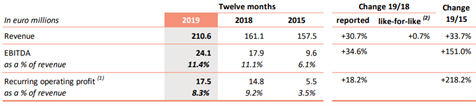

Fashion Technologies: the PCC success story that keeps on giving

With the integration of PCC being fully realised, the division posted another strong year. Profitability remains solid at 8.5% in spite of the negative effects related to the devaluation of the Argentine peso and increased opex related to the premiumisation strategy. Among these investments is the development of a ‘green’ product offering to cater to fast-fashion brands.

This comes at a crucial time as these brands rush to implement eco-responsible materials in their value chains in an effort to mitigate the major ecological impact behind the fast-fashion industry. This high value-added offering is bound to improve profitability and, coupled with the sales volume increase from integrating PCC Interlining, the division has the potential to overtake Protective Films as Chargeurs’ prime cash cow.

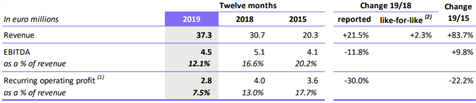

Museum Solutions: An out-of-the-box transformation story

In its previous form, the ex-Technical Substrates business was primarily a conventional industrial affair. Starting with the 2018 acquisition of UK-based Leach, the division has seen a surprising transformation into a one-stop shop solution for museum services and exhibitions. In late 2019, the leap into the US through the acquisition of the US market leader, D&P Incorporated, marked a major step in Chargeurs’ pursuit in this unconventional high-growth niche.

Regarding the FY19 results, the sales boost was mainly explained by the integration of Leach and to a lesser extent to the consolidation of the results from Design PM and MET Studio, which will team up with D&P and Hypsos (acquisition currently undergoing) to offer top-end know-how for museum and exhibitions, targeting the increasingly important “visitor experience”. Chargeurs highlights that growth in emerging markets is also a major potential driver for the division. The group expects recurring profit to stand above 10% in 2020, while turnover will cross the €100m milestone much earlier than anticipated.

Luxury Materials: now worthy of its name?

Being familiar with Chargeurs’ historical Wool business, the move to rename it into ‘Luxury Materials’ came across as very aspirational in nature. The weighty luxury stamp may have well been earned, as the transformation of the business (which management highlights was made at a low cost) to move it up-market appears to have borne fruit. The focus on ‘traceable fibres’ has now become a major trend in the world of sustainable fashion. This has allowed Chargeurs to get closer in the value chain to the luxury brands that use their products, instead of wool spinners (which has been the historical customer base). Profitability remains quite modest but we find the value proposition nonetheless enticing.

We will integrate the 2019 results into our model and roll forward our estimates for 2022. The FY19 sales came just slightly below our forecasts, and are overall good considering the volatile market environment. We will trim our operating margin expectations for the Protective Films division as the highly profitable Chinese and German markets are likely to continue showing weakness in the context of the COVID-19 outbreak.

On the other hand, we will bump up our expectations for the Museum Solutions division as management is confident of attaining a >10% recurring operating margin in 2020. We continue believing in the long-term outlook for the group as demonstrated by management’s ability to transform its main businesses and attain leading positions in its respective markets through strategic acquisitions and a focus on high-value offerings.