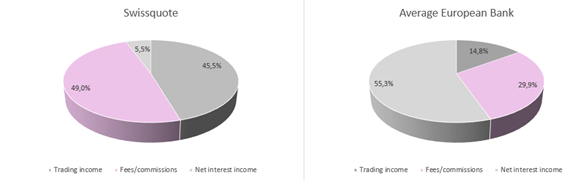

Like any other bank, Swissquote makes a profit via net interest income (NII), fees/commissions and trading income.

Contrary to traditional banks, which make the bulk of their revenues through only net interest income, Swissquote’s net banking income is mainly supported by fees/commissions (through the securities brokerage) and trading income (the FX activity).

Traditional banks’ main activities are more particularly focused on loans and mortgages. Swissquote offers mortgages but acts only as an intermediary and will earn a retrocession on NII from the mortgages issued. It indeed delegates the issuing of the loan to a partner (the Basellandschaftliche Kantonalbank) which will use its own balance sheet. Swissquote’s NII relies mainly on its retail deposits which are then invested (cash and balances with the central bank, treasury bills and due mainly from banks).

In a normal configuration, the level of NII is positively correlated to the level of retail deposits (it mechanically increases as the retail deposits base increases). However, the current abnormal level of interest rates (negative or very low at best) questions this.

Negative rates as a drag on NBI

The impact of negative rates was particularly penalising for Swissquote some years ago when it made between 25% and 35% of the group’s total revenues (25% in 2007). Remuneration on risk-free assets has been negative in Switzerland and Europe for some years now. It gets positive remuneration only in the US where rates have only been under pressure again since the beginning of 2020 (long-term rates have been sharply decreasing after the pandemic rattled the economy in March 2020). Fortunately, the company has managed to diversify its activities geographically by business division with the consequence of reducing its dependency on Swiss interest rates.

According to the company’s financial reports (2020 annual report), a 100bp increase in CHF, EUR and USD would add about CHF22m to the group’s operating profit (a 22% increase to Swissquote’s 2020 operating profit).

Swiss banks have been amongst the first to impose a negative remuneration on private deposits to curb the impact of negative rates on the assets side. This makes sense, as loans and their remuneration (NII) are core to their business…

Swissquote has been charging negative rates for clients with deposits over CHF500,000 (CHF250,000 or CHF100,000 for some Swiss banks). Indeed, it does not want to be misused to park money (so clients avoid negative charges at other banks). Clients are offered free trades (Swissquote’s core business) as compensation.

Net interest income makes now (in 2020) only 7% of the company’s total revenues and management’s (bullish) guidance for 2024 did not factor any increase in rates.

Swissquote’s biggest contributors to its revenues are indeed fees/commissions when investors trade on its investment platform and trading income that is mainly gained from online foreign exchange transactions (and from foreign currency translation of monetary assets and liabilities denominated in other currencies than CHF).

A risk in Swissquote’s business model is therefore its dependency on financial markets’ activities. Contrary to traditional banks, whose loans business guarantee them recurring revenues on a long-term horizon (roughly equivalent to the loans’ duration), the Swiss Fintech has to face the upheaval in financial markets (leading to some revenue volatility). Hence, the need for assets and geographical diversification. And here Swissquote has some history of external growth (which adds to organic initiatives).

Growing to diversify

As we mentioned in the previous section, Swissquote’s main growth engine is its B2B solution. It indeed enables the company to leverage its tech-oriented trading platform at a very low cost. On the other side, it has been investing to increase geographic coverage (add exchanges) and add new asset classes (such as Swiss DOTS and cryptocurrencies as the Swiss Fintech was the first bank to allow its customers to trade cryptos in Switzerland).

Its main achievements were indeed the launch of the FX platform (eforex) in 2008, which makes, as of today, 30% of total revenues, and the launch of Swiss DOTS, an OTC platform that enables investors to trade OTC-leveraged products offered by the big global banks. These benefit from softer constraints compared with the highly regulated SIX Structured Products exchange.

The last lucrative development is the infrastructure set up around crypto-currencies trading and which has enabled Swissquote to be well ahead of its competitors (traditional or low-cost brokers). The institutionalisation of crypto-currencies trading could therefore be Swissquote’s next engine.

Swissquote has indeed been offering crypto-currency trading services since 2017 (supporting five currencies, amongst which Bitcoin and Ether). In October 2018, the bank expanded its service to enable its clients to participate in initial coin offerings (ICOs). Since March 2019, the Swiss Fintech has also offered its clients the opportunity to centralise their holdings of crypto-currencies, as it is possible to transfer crypto-currencies from external wallets to a Swissquote account (and vice versa).

At the end of 2020 and beginning of 2021, crypto-currencies trading has been institutionalised and the impact on Swissquote’s revenues should be more sustainable than what it was in 2018.

Some volatility should obviously remain around this alternative asset class but offering this opportunity to investors positions Swissquote ahead of its competitors.

Swissquote has also expanded through external growth. The Fintech’s first big acquisition was in 2002 when it bought Consors’ Swiss business. This business focused on B2B business (asset managers). Since 2002, Swissquote has therefore obtained experience in serving asset managers through a dedicated trading platform (Swissquote Professionals). MIG Bank in 2013 (FX) was another notable acquisition.

And Swissquote is active again as it finalised in H1 19 the acquisition of InternaxX. Through this acquisition, Swissquote has unrestricted access to the European market, meaning it will drastically increase the range of investment solutions it can offer its European investors (it will also expand InternaxX’s service offering with a greater range of products).

Swissquote Europe bank (former InternaxX) had €2.6bn AuMs in 2020 in Europe. The Swiss bank plans to attract about CHF2.5bn net new money per year until 2024 outside Switzerland with the bulk in Luxembourg. Assets in Luxembourg should therefore be about CHF8bn in 2024.

Swissquote targets customers there who have about €100m in assets, like in Switzerland. It is therefore competing rather with the big banks and private banks by offering the “Swiss” quality and safety in Luxembourg (it does not compete with Flatex in Germany for instance).

As part of its international development, Swissquote has also opened a subsidiary in Singapore where it intends to develop business for asset managers (offering also nine new online stock exchanges to its investors).

With a solid current CET1 ratio (about 800bp or about CHF140m excess capital), we expect the company to continue with acquisitions to leverage its trading platform internationally.

More projects in the pipeline

The accelarated development of the crypto-currencies eco-system is not Swissquote’s sole project in 2021. The Swiss Fintech has indeed set-up a joint-venture with the Swiss bank, Postfinance, to compete with the most notable Fintechs such as Revolut of N26.

The idea behind the JV is to use Swissquote’s expertise in digital banking/financial services and also leverage Postfinance’s big network. Guidance for 2024 does not factor in this project but it should probably add to the company’s bottom line in the end.

As a savvy Fintech, Swissquote has also recently developed a new online leasing offering for customers willing to own a Tesla with a target volume of CHF100m in 2021.

Swissquote has also been promoting its own multi-currency credit card. It represents in Switzerland a better alternative to credit cards proposed by traditional banks as fees charged for transactions abroad are close to 300bp in this case. On the contrary, like Revolut or N26, Swissquote offers a much cheaper alternative for these kinds of transactions (0% fees and a real-time rate). These types of solutions mostly appeal to millennials who are comfortable with 100% digital solutions.

Swissquote’s number of engineers (250) make up about 30% of the headcount which underlines the importance of innovation for the company.