In a display of astute and agile management to face the difficult market context brought about by the pandemic, Chargeurs closed a successful FY20 with record profitability. This was driven by the group’s new personal protective equipment venture, in addition to a solid rebound at its core Protective Films division. Parting from an improved scenario in 2021, the group now looks forward to its ambitious 2025 objectives which put a bigger focus on nurturing lfl growth.

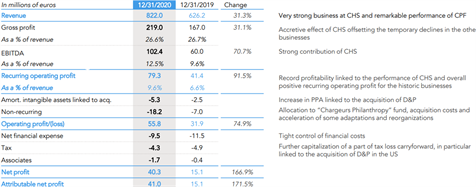

Chargeurs had already released its group revenues for FY20 in January, figures that came in slightly below our forecasts (-2.3%). Meanwhile, the recurring operating result came in 4.5% above our forecast, reaching €79.3m, a historical high. The outperformance was driven by a stronger than anticipated profitability for Chargeurs Healthcare Solutions (CHS), which achieved an operating margin of 20.9% versus our 19.1% estimate. The operating performance for the group’s historical businesses fell in line with our expectations.

The descriptive P&L provided by the company, shown in the table below, clearly displays the different drivers behind the FY20 record result.

With regards to the group’s net debt position, there was little change as it increased just slightly from €122.4m in 2019 to €126.7m at the close of FY20. This coupled with a record EBITDA of €102.4m, driven by the strong operating results, led to a 1.2x net debt/EBITDA ratio, putting the group on a solid stance to execute its new strategic plan with a 2025 horizon.

The notable results have been accompanied by a notable dividend, jumping from €0.40 per share last year to €1.32 per share on the FY20 earnings (of which €0.28 has already been paid as an interim dividend).

Looking at Chargeurs’ FY20 release, we have to recognise the feat achieved by the group’s management, which was capable of turning an adverse context into an opportunity to create a novel business line that will now stand as the fifth pillar behind the group’s newfound organic growth ambitions, as it turns the page from the previous Game Changers strategic plan. It is also an accomplishment that Chargeurs exits a turbulent 2020 with a more solid financial standing, while funding two tactical acquisitions adding the final flourish to complete the group’s “one-stop-shop” Museum Solutions division.

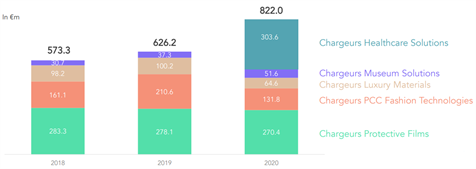

Divisional revenue breakdown

Source: Company reports

Protective Films’ strong Q4 20 bounce-back boosts 2021 outlook

Taking into account the very challenging trading environment in the CPF’s main markets for a better part of last year, the division was able to recoup most of the ground lost, closing the year with revenues of €270.4m, only -1.8% lfl below the 2019 level.

Profitability was also relatively resistant, as CPF’s products are an essential part of industrial supply chains worldwide, while its high-end market positioning helps diminish margin erosion. The decline was modest with the recurring operating profit margin falling from 8.5% in 2019 to 6.3% (€17.0m) in 2020. The resilient operating result should lead to a material improvement in 2021 as volumes recover to their pre-pandemic levels.

Fashion Technologies: fashion sector woes weigh on results and near term scenario

Due to its exposure to the fashion sector, which was hard-hit by the pandemic and the lockdown restrictions that have significantly curtailed the activities of fashion retailers, the division could not escape the drag on revenues and earnings that stand out as the “chip on the shoulder” of an otherwise positive end to the year. CFT-PCC saw its revenues fall by 35.3% lfl in FY20 to €131.8m, and recurring operating profit shrunk from €17.5m (8.3% margin) to €5.1m (3.9% margin).

Unlike CPF, the 2021 outlook for Fashion Technologies remains challenging, with management being transparent in that we will not see a return to the pre-pandemic levels in the near term. The focus this year should be in safeguarding profitability in the context of structurally-lower volumes, hence we see profitability improving to a 6.2% recurring operating margin in 2021.

Museum Solutions: New additions offset technical substrates weakness

The division’s FY20 results were a contrast of the serious impact of the sanitary crisis on the activities of the legacy business and the good performance of the newest additions serving the niche of museum servicing and solutions. Regarding the former, the poor retail environment provoked by lockdowns and social distancing measures led to a decline in demand for publicity and posters in retail stores, while the complete lack of expo shows meant a double-blow to the main end-markets for the technical substrates business.

Meanwhile, Chargeurs roster of museum-focused businesses continued securing important contracts that should bring good visibility for the near team. Overall, this resulted in revenues falling 47.5% organically but increasing +38.3% reported to €51.6m. Recurring operating profit came in at €1.9m (3.7% margin).

Healthcare Solutions: Remarkable profitability was a welcome surprise

While we had already recognised the accomplishment of the €303.6m revenue contribution from Chargeurs’ newest division. The real cherry on the cake was the exceptional profitability shown by a division that did not exist at the beginning of last year.

The 20.9% recurring operating margin stood above our already bullish (in our view) forecast. While the commercial success of its line of PPE products was facilitated by the unprecedented sanitary context, the fact that management was able to draw significant cash generation (recurring EBIT of €63.5m) out of existing assets should be applauded. Moreover, the division was built up with a minimal need of capital employed, as the latter remained basically stable compared to the group’s 2019 level.

Although the breakthrough performance seen in FY20 is not likely to be replicated in FY21, as the pandemic is brought under control through the current vaccination efforts, Chargeurs’ confidence in CHS reaching €50-100m in turnover this year shows that the company has been able to build a strategic asset that will support the group’s growth ambitions, as outlined by the targets in its new strategic plan.

New strategic plan shares acquired growth and lfl growth ambitions

The publication of the 2020 results also marked the occasion for Chargeurs CEO, Mr Michael Fribourg, to present the roadmap that is set to guide the group over the next five years, dubbed “Leap Forward 2025”. While the pursuit of acquired growth characterised the previous strategic plan, now that the group has been able to forge five divisions anchored in five distinct niches with solid growth potential prospects, the role that organic (embedded in Chargeurs’ lingo) growth will be ever more important for it to reach is 2025 targets.

The group aims for €1.5bn in revenues by 2025, with a target profitability of 10%, corresponding to €150m in recurring operating profit, compared to a “normalised” 2019 level of €49m. The roughly €100m in additional recurring profitability is to come in equal parts from lfl growth and acquisitions. Debt should remain relatively stable (currently standing at a 0.5x equity gearing ratio). We see these objectives as a reassuring continuation of a strategy that has served the group well, as evidenced by the satisfactory performance in the midst of a sanitary and economic crisis.

Our model is currently under revision as we incorporate the FY20 figures and we roll forward our forecasts until 2023. We maintain our positive stance on the stock.