Cementir is remunerative because it is a specialist in a niche business too small for mega players to invest in. Scarce raw materials command higher prices and, as a result, white cement can be exported, which is unusual for construction material commodities. While part of the higher realisation prices is absorbed in higher energy costs, the business is intrinsically a better FCF generator than the grey variety. The company appears to have been nimble in expanding by acquisition, expanding its network (and thus its logistics efficiency), to have been careful about capital spending and good at running a mid-sized operation. The obvious limit is that with already 20% of the market, growing more rapidly than the market is likely to entail declining ROCEs.

A business model somewhat similar to Sika’s and Imerys’

Sika’s ad-mixtures added to concrete represent less than 1% of the value of the final product, but give added functionalities such as accelerated curing of concrete which can lead to cost savings. Similarly, Imerys’s speciality minerals represent a small cost in its customers’ final products (between 0.5% and 7%) but are strongly value-added with low substitution risk.

Knowing that cement typically represents less than 5% of the construction costs and that white cement has much more functionalities/applications than grey cement, one can focus on the intrinsic positives of white cement, keeping aside its cost.

Concerning raw materials (26% of total operating costs), Cementir is vertically well integrated in the grey cement sector. For white cement, it is clear that suppliers have a stronger bargaining power, which explains why the focus of Cementir has been on integrating vertically in this sector.

Even if white cement is principally a B2B business, the bargaining power of customers is low. Price sensitivity of white cement is low and switching cost is high. The number of customers is high, while the size of each customers’ order is rather low.

Cement does not see new entrants due to capital intensity and regulations (tougher on emissions). For white cement, this is compounded by a B2B-only profile. White cement tends to be sold to dry mix manufacturers which have very high specification standards and significant quality and consistency requirements. Once a supplier qualifies, it is then expensive for the customer to switch to another supplier, making it a rare option.

Grey cement business model

Grey cement is capital intensive, local and relies a lot on the good control of local markets, most notably through the good positioning of ready-mix units. Vertical integration is thus essential but limited to countries where Cementir has a grey cement exposure.

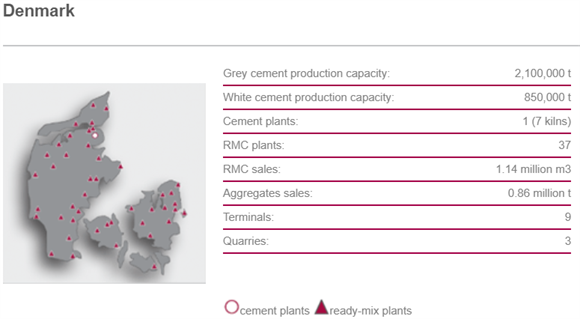

As the markets for cement are local, location and diversification are key to value creation. A presence near a developing city is a necessity. Indeed, urban markets are a strength, especially in view of the growing urbanisation trend in developing countries. Cementir has a significant local market share in each country that it is active in. For instance, Cementir owns the sole operating cement plant of Denmark. So the market share is pretty high, as the only competition is from the imports.

In other countries, such as Turkey, the market share is low (<5%), but the plants are located where competitive pressure is lesser than usual (see figure below). So the local market share with a 100km radius is expected by AlphaValue to be several dozen percentage points higher when it cannot be considered as a local quasi-monopoly.

Expedient businesses

The other construction materials and services business, which consists mainly of ready-mix concrete, has a very low margin. However, it is of strategic importance because the ready-mix concrete business acts as a distribution channel for cement and aggregates products, with the end goal of increasing the sales volume of the other two divisions which have significant margins.

Controlled leverage through the cycle to catch opportunities

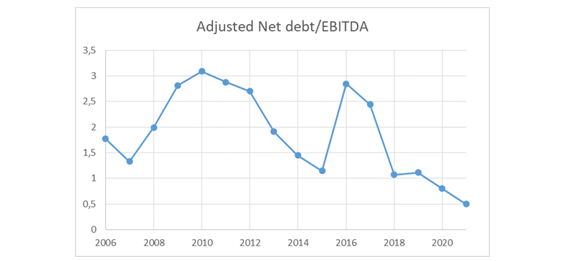

Cementir’s leverage has remained between 1x and 3x through the cycle. This is quite commendable and raises hopes for future capital allocation. We see a parallel with Vicat’s indebtedness, which makes us believe that family-driven businesses are unwilling to take risks and this is positive in such a capital intensive and cyclical industry.

As for capital allocation, in slowly growing industries, M&A is key. Even though Cementir has set its eyes on digitalisation and sustainability, the possibility of M&A activities cannot be discarded. We presume that Cementir’s next phase could be to expand further in the grey cement market in order to dilute its exposure to Turkey in terms of cement capacity and to increase the global reach of the company.

Operational excellence

Lower energy prices a key driver of EBITDA margin growth in recent years

The decrease in energy costs has acted as a tailwind for the cement industry since the sharp fall in oil prices which began in 2014. We expect energy prices to remain at the current low level.

Should energy prices rise again, Cementir is safer due to its exposure to white cement, where price hikes are easier to pass on to customers.

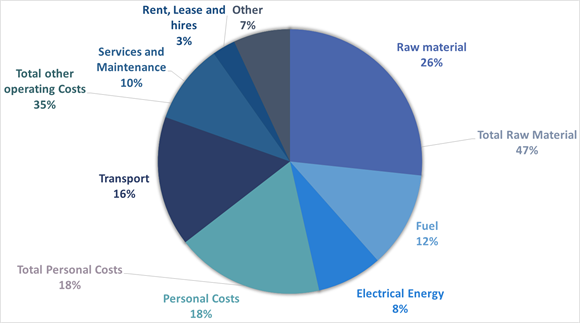

Below is a pie chart with the cost structure of the company in 2018. As usual in the cement sector, raw materials and energy (transport included) take up most of the cost structure (two thirds), while employee and opex make up virtually all the rest.

Cost structure of the company in 2018

Capital allocation

Through 2006-18, Cementir invested about 10% of its sales in capex, with ups (22%) and downs (6%) linked to the stage of the economic cycle but to a lesser extent than peers, which means that this company navigates successfully in a capital-intensive industry.

Since 2006, the group has been making remarkable cuts in capex. Capex as a percentage of depreciation went from more than 350% in 2006 to about 50% in 2010, underlining that a period of under-investment was thought as a better way to protect the company over the long term by management, before rising back to some 90% in 2019. The likelihood of expanding the group’s activities will be more in grey cement than in white cement. Indeed, with the current 20% market share, it will be hard for the company to increase it further without raising anti-trust concerns or declining ROCE.

Contrary to peers, Cementir did not over-invest in acquisitions during the economic boom of 2007 to 2008. This demonstrates management’s temperament and substantiates the fact that Cementir’s management is exemplary.

Value creation

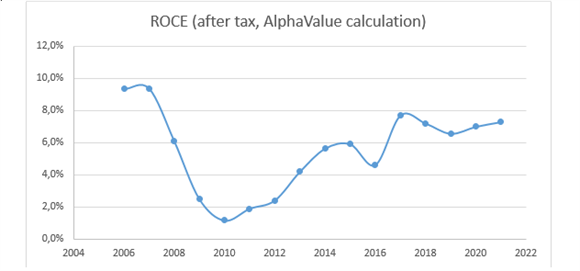

One of the most resilient cement companies in the financial crisis

Cementir is one of the few cement companies to have seen its net profit remain positive all through the cycle. On top of this, impairments, when needed, were controlled and reasonable (maybe with the exception of Italy as it was sold at a loss).

Cementir’s ROCE at 7.7% (2017) and 7.2% (2018) have been higher than the average of peers (6%). This is not enough to meet the cost of capital in AlphaValue’s computations, however. This is partly derived from AlphaValue’s defined risk free rates and equity risk premium which when combined at 8.5% stand somewhat above what corporates may use. While Cementir does not provide a breakdown of its WACC, we understand that it is value creative on this front.

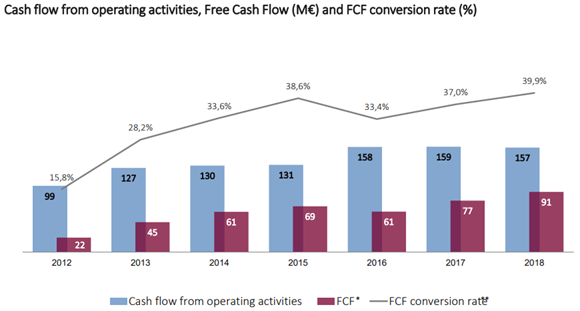

Cash generation is satisfactory as one can see that the FCF conversion rate increased from 16% in 2012 to 40% in 2018, a performance that we expect the company to increase further over the long term.