It has been known for a while that Swissquote is not just a regular online retail broker. In our view, however the market has yet to really price in the full potential of its platform. 2022 was a tough year for financial markets (and alternative asset classes like cryptos) but, despite this, Swissquote demonstrated its resilience and ability to dodge market turbulence. In our view the firm is a ticking bomb of hidden value waiting to be triggered by better market sentiment.

Apart from its retail brokerage business, Swissquote has numerous assets that need to be considered in valuation.

The valuation paradigm needs to look beyond this core business and consider the following:

- Swissquote without the crypto business is not fully priced into the current market capitalization

- The firm has built a crypto exchange which has immense potential value

- Swissquote is building a platform at the crossroads of the likes of Moneyfarm, Revolut, Avanza

- The firm captures the higher interest rate environment, naturally hedging the financial market exposure

Swissquote with and without cryptocurrencies

Swissquote has a great asset compared with many online retail brokers; it offers cryptocurrency trading. While this may not be the most powerful argument these days, one should not forget that markets are fickle and this may turn out to be a major plus were the hype to return.

Nevertheless, given the uncertainty concerning the future of this asset class, it is worth looking at Swissquote’s underlying value were cryptocurrencies to disappear.

As we are attempting to solve an equation with unknown multiples, a key parameter in our reasoning comes from the firm’s highly disciplined cost base management.

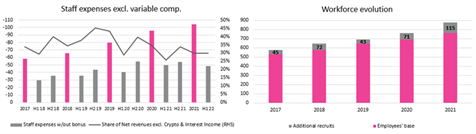

Let’s start with staff costs, from which we exclude variable compensation in that the latter contributes noise which is unhelpful in terms of ringfencing the ongoing payroll expenses. Cross-checking with recruitment enables us to identify the recruitment effort and the amount of the CHF impact on the firm’s budget.

There were major recruitment drives in 2018, 2020 and 2021. In 2019 the firm’s payroll costs peaked as a percentage of net revenues, excluding Crypto and Interest Income-related revenues. This is consistent with the firm’s discipline and ability to predict the revenues that it will generate, and to adapt recruitment accordingly. (We exclude crypto-related revenue in order to isolate the cost impact of recruitment on the “regular” business margin and interest income-related revenue as we believe it is independent of the workforce).

To derive crypto-related payroll costs, we have assumed that a company like Swissquote grows its staff cost base by between 10% and 15% a year (recruitment plus salary increases). However, since the past 3 to 4 years have seen the rise of online retail brokerage platforms (due to increased interest in financial markets, COVID-19, willingness to invest in a supplementary pension, etc.) and this trend looks set to continue, we take the view that the firm has leveraged this massive increase in commission-based revenue to also increase its recruitment effort for the “regular business”.

Hence, our scenario takes in a growth assumption of 20%, and identifies any costs above this as having been incurred to develop the crypto-related activities.

Running this scenario from H2 19 to H1 21 (the period during which crypto products were launched and deployed) points to c.CHF10.2m of staff costs, excluding variable compensation, to run the crypto product. There will have been other expenses before and after this window hence we would assume c.10% more costs leading to c.CHF11.2m in FY 21 (which represents c.10.8% of total payroll costs without variable compensation). Assuming that these employees earn c.15% more than the “historical” workforce (scarce engineers and developers with rare backgrounds), this would imply c.63 people at Swissquote working on crypto-related matters (c.6.7% of the average number of employees in FY 21).

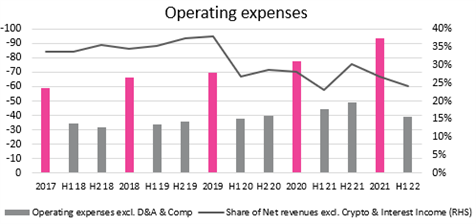

Looking at operating expenses excluding Depreciation & Amortisation and Staff costs, we can see the same discipline across the board.

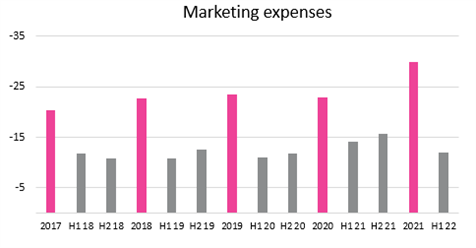

The operating expenses line includes marketing expenses and provisions. For marketing expenses, in our view it doesn’t make sense to differentiate a marginality given that the firm’s marketing expenses mostly promote Swissquote as a whole rather a given product area. Moreover, we can see from the trend in marketing expenses that, again, the firm has a very disciplined spending policy with flexibility depending on whether nor not any one year is lucrative.

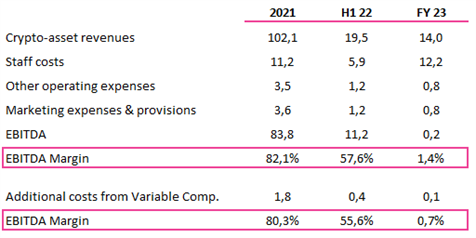

However, we can see that other operating expenses increased during the peak crypto period (2020 and 2021). It is hard to tell whether these incremental expenses are fully dedicated to products or simply the overall business growth (in 2020, net fee & commission income rose by 68% yoy) however, given the sustained expenses in 2021 while Net fee & commission revenue grew by “only” 10% (and crypto by 537%), and in line with our previous comment on staff costs (the firm having used the huge increase in volume to fund additional expenses for the “regular” business) we would assume that, in 2021, there were CHF3-4m of expenses generated from cryptos, although this spending remained mostly variable.

Adding up the numbers, we derive a kind of EBITDA, in which we divide the marketing expenses & provisions by 5 (number of revenue lines of Swissquote) and further divide this number by 2 assuming that these expenses are for the overall business. For H1 22, we assume staff costs growing by 5% yoy (mostly driven by wage inflation) and other operating expenses and marketing & provisions divided by 3, given the expected lower effort on advertising cryptos.

Our assumptions for FY 23 include staff costs increasing by 4% yoy due to inflation and people rotation (we can see that, since FY 21, the average wage per employee, calculated using the average number of employees throughout the year, is trending downwards, assuming a cheaper people rotation considering the increased recruitment efforts), then further cut the other operating expenses and marketing expenses vs. FY 22.

Our assumptions suggest that cryptos were highly accretive for the EBITDA margin in 2021 and very slightly accretive in the H1 22. However, we expect the crypto business to be barely profitable in FY 23.

Excluding cryptos, any incremental profitability for Swissquote is more than offset by higher interest income, despite conservative assumptions for commission income in FY 23.

Applying a conservative 23e EV/EBITDA multiple of 11x to Swissquote’s business excluding crypto, we derive a CHF3.05bn valuation (above the firm’s current market cap). Applying a multiple of 3x EV/EBITDA to the crypto business for the average FY 23-25 EBITDA (a lower multiple as we believe the firm would be able to cut fixed costs if the activity remains unprofitable), we derive a negative CHF9m. Deducting the Net Debt – or rather an expected net cash position of CHF 464m for FY 23 – Swissquote would be worth c.CHF3.5bn based on a SOTP methodology.

Swissquote’s rejected asset

The crypto asset class is not what investors want to hear about these days given the recent scandals but, in our view, it would be unwise to wave cryptos goodbye. While, as we have seen, were cryptos to disappear, the downside for Swissquote remains limited, the upside opportunity is immense.

Should the hype return, Swissquote has built an immensely scarce asset: a crypto exchange.

Swissquote has hitherto been using the Bitstamp and Coinbase exchanges as liquidity providers for crypto trading as well as custodian services. This means that, for any order sent by a Swissquote user to buy BTC or ETH (among others) on the platform, the order would be re-directed to the Bitstamp or Coinbase exchanges. This has meant potential friction, reliance on external providers (potentially decreasing stability) for execution and liquidity, and dependent upon their regular maintenance.

This has also meant commission for trades (0.5% to 1%).

With its own exchange, which at first will be rolled-out to Bancor (BTN) and progressively to all 36 tokens available on the Swissquote platform, the product should considerably improve.

Summed up another way: getting rid of an exchange and becoming this exchange is crazy.

Business model developments: what others look like

The market has had difficulty in valuing Swissquote which claims to be different from a classical online retail broker while not being another neobank.

As the business develops and market participants emerge, Swissquote’s value and uniqueness become clearer as it seems to aggregate parts of many highly-regarded firms of which two are rarely mentioned: Revolut and Moneyfarm.

Swissquote’s underlying value thus remains immense when looking at the peer valuations for similar services. Add to this the fact that Swissquote aggregates all these services on its own platform and the shares definitely deserve a premium given the trend towards super-apps and the powerhouse they represent.

We’ll be watching for further developments, but our money would be on Swissquote not stopping here. If it manages to record regular inflows/outflows on the back of its payment cards, pushing users to think of their trading account as a kind of regular account with the flexibility to bring-in/withdraw funds, these flows could become very valuable, and trigger a new perception of investing and consuming.

Accumulated dry power to be lit in a few months

Swissquote has built an extremely well-balanced business. What it has lost in the financial markets (and cryptos) in recent months has been fully offset by the higher interest rate environment. A natural hedge that deserves a premium.

Swissquote continues to accumulate users on its platform and we believe that this huge growth in accounts (18.9% in 2021 and 13.5% in H1 2022) is going to feed additional “new monies” as users progressively gain trust and adoption of the app increases.

An impressive volume of trades and activity is expected as soon as market sentiment improves across all asset classes.