Dolfines has two divisions which ensure most of the current revenue (Factorig and Services), another two divisions which are lumpier and more dependent on exploration and production spending (Solutions and Contracting), and one wild card division with high growth potential (New Energies). Lastly, 8.2 France, now part of Dolfines, has shown strong growth in recent years and is supported by the dynamic wind market.

Oil & Gas

Services

The company has a vast network of qualified manpower that it can send to production sites around the world on an individual basis or as a multidisciplinary team. Customers are exploration and production companies and larger oil and gas services companies. Typically, the customer will contract the workforce for a specific mission, but Dolfines also has several multi-year agreements with long-standing clients.

Providing a technical workforce is a high volume, low margin business. Contractual prices for assistance and temporary manpower are competitive in the oil and gas industry and this is a fragmented market with low barriers to entry. EBIT margins can reach 6-7%, higher than generalists in workforce solutions (Adecco has an EBIT margin of c.4.5%), reflecting the specialised talents Dolfines can provide.

Dolfines uses its network and technical knowledge to allocate its team around the various projects in which it is working on. A higher number of contracts allows for optimisation of manpower and usually improves margins when talents are in demand. The strength of Dolfines in this activity is its ability to recruit talent on a timely basis (and avoiding costly inter-contracts).

We expect the trend in manpower outsourcing to continue in oil and gas, especially on operational activities, due to the nature of exploration and production which requires specific competencies at each step of the project.

Factorig

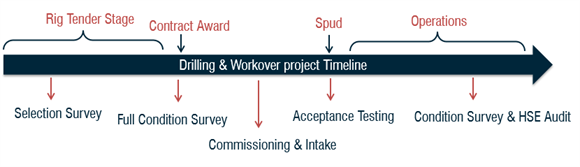

Dolfines is an independent third-party rig and QHSE (quality, health, system, and environment) auditor. It assists oil and gas contractors in reducing their operational risks. Works include full condition surveys once the rig has been delivered to the client, rig inspection during operation, inspection of new equipment prior to its integration, etc. The Factorig division is based in Abu Dhabi and has a strong presence in the Middle East.

The company can recertify blow-out preventers (BOP). It has both ISO9001 and API Q2 certifications, which are crucial quality management system requirements for contractors. A BOP is some safety equipment which is used to hold well pressure and prevent uncontrolled flow.

Inspecting and auditing a rig is a recurring business that occurs throughout the whole lifespan of the asset:

In addition to rig inspection, the company can also recertify BOPs from Shenkai.

The BOP recertification market is a good addition to the Factorig division. Safety regulations have increased after the Macondo oil spill in 2010, at which the BOP failed, with BOPs recertification occurring every five years. BOP manufacturers are strongly incentivised to stick to safety requirements. As a reminder, Cameron International Corp, the BOP manufacturer for Macondo well, agreed to a $250m settlement with BP in 2011.

Good execution from Dolfines on the Shenkai BOPs could give them access to partnerships with additional BOP manufacturers.

The Factorig division operates in a niche market where EBIT margins could be c. 20% in an upcycle, with customers that are not likely to switch from one contractor to another. The recurrence of the activity associated with customer retention gives audit and inspection a singular and attractive feature within oil services.

Solutions & Contracting

Dolfines is at heart a firm of engineers and has a good track record, with projects realised for various contractors (mainly European and Middle Eastern companies).

Contracting: Dolfines provides project management and services throughout the whole lifespan of a rig. It is focused mainly on complex drilling operations, using the expertise of its other divisions to offer an integrated solution to its clients.

Solutions: This is Dolfines’ engineering unit. The company has been involved in many projects, including the designs of rigs that required ad hoc specifications and studies on modular cluster rigs. It also has expertise in offshore with designs done on jack-up rigs, tender-assisted drilling barges and swamp barges. The Solutions division also offers technical support to the Factorig and Services divisions.

Its size makes it less vulnerable to bigger engineering firms (such as Technip Energies and Saipem) as it will compete for smaller projects and will typically serve those contractors when it can bring its expertise (such as rig reactivation services).

There is also hidden value with having the engineering division located at the headquarters and providing technical support to the units abroad. For instance, Dolfines has done an engineering study to upgrade a rig for Perenco that required a BOP system. Dolfines can participate in these types of projects thanks to its API Q2 certification and the engineering branch.

New Energies

Business model

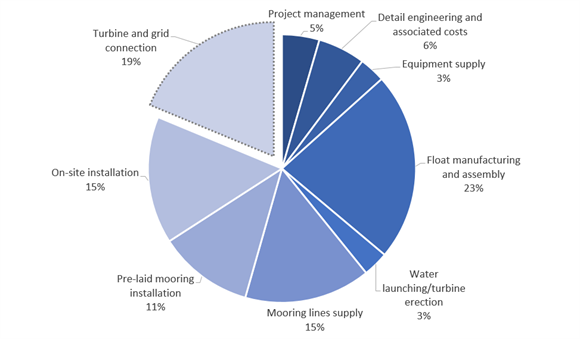

Dolfines will be contracted by developers. The scope of Dolfines’ activities can vary according to developers’ needs. Dolfines’ responsibilities can include:

- project management (project follow-up including construction and installation);

- detailed engineering (engineering, licensing, software, certification);

- supply of equipment (ballasts, crane, chain connection, power generation for installation);

- on-site installation (towing, mobilisation, connection to pre-laid moorings, supervision);

- supply of mooring lines (chains, anchors, buoys, shackles);

- water launching and provision of the yard during the erection of the turbine.

With regards to the construction of the floater, several solutions are being envisioned. The first one is a joint venture where Dolfines doesn’t earn fees on the construction contract. The second one is where Dolfines handles the entire process (float and BOP) under the form of an EPCI contract. The third one is on commercialising the offering throughout licensing to a larger Engineering, Procurement & Construction (EPC) contractor, rather than on Dolfines handling the procurement and construction (on top of the engineering and design). In our view, this option is justified as Dolfines now targets a floater that can support a 15MW turbine, with a potential order intake that could be large and executed by an EPC company. The total cost of an installed unit should indeed range between €30m and €35m for an order of one unit only, while prices for bigger orders are expected to be reduced by c.€3-4m. We expect that a licensing contract should range between €250k-300k per unit.

Total cost breakdown, for one unit

Source: Dolfines, AlphaValue estimates

Like in any nascent, high potential market, we expect margins to remain relatively low during the first years as the company invests in research & development. We then estimate a 60% EBITDA margin due to the light asset base (provided that Dolfines sells on a licensing basis). This is similar to GTT’s business model (and margins) which designs and engineers membranes for LNG carriers.

Capex is expected to remain modest given the lightness of the business model. We forecast small intangible investments, mostly software licences in the vicinity of c.€12k per year and per employee. As for the number of staff, we use Dolfines’ estimates of five employees per unit ordered, for pilot and small wind farms, and fewer employees per turbine for bigger orders as the their scale allow for some cost reduction.

Risks

The main risk comes from timing and competition as Dolfines’ main competitors are several years ahead in terms of developments. Principle Power Inc. has already tested and decommissioned a full-scale 2MW prototype of its WindFloat design. Ideol’s first demonstration (Floatgen) became operational in September 2018 and has already been delivering power to the grid since then. SBM Offshore is developing Provence Grand Large with EDF Renouvelables.

Another disadvantage could be Dolfines’ own size as the company’s current revenue is lower than the price of a single floater. Therefore, the development of the New Energies division will be limited to pilot and small-scale wind farms during the first years and bigger developers are likely to prefer to wait to see the first unit in operation before placing large orders.