IDI is a pioneer in the private equity arena in France, with over 50 years of experience in the field and a particular investment focus on SMEs. IDI is one of the first listed investment companies in France (1991), achieving an annualized IRR (dividends reinvested) of 15% over the past 30 years. IDI’s NAV has grown significantly over the years and is now approaching €700 million, with an average discount of 30% observed since 2014.

IDI strikes as a private equity firm effectively more aligned to the interests of its stakeholders than the industry mediocre record in that respect. This is in spite of its resorting to a partnership limited by shares as a legal shell. IDI differs as it has no time constraint and as its management has skin in the game at the holding level as well as at the equity stakes level. Indeed, what sets IDI apart from other private equity players, aside from the fact that most of the investment activity is funded by its own equity capital, is that it operates under a model that is not constrained by time to liquidity that most PE funds are subject to.

On the one hand, this flexible approach allows IDI to accompany the investee companies through the whole development process without having to resort to hasty value-pumping measures in order to appease investors waiting to be paid out. On the other hand, the liberty of not having to adhere to a calendar also allows the company to be agile and seize opportunities when they arise. This may result in IDI exiting investments faster than its more usual investment horizon of five to seven years, to capitalise on favourable market conditions and crystalise higher IRRs.

A resilient flexible investment approach in the face of a crisis

This no-rush approach is conducted by a management team that, all combined, makes up the main shareholder base, accounting for 55% of the share capital, providing plenty of confidence that the company’s equity capital is being allocated wisely in order to support long-term value creation. The lack of a liquidation schedule also allows IDI to time its exits better in periods of market downturn — as was the case in 2020 at the height of the Coronavirus pandemic — to capitalise on a subsequent recovery in market multiples to crystallise higher rates of return.

Demonstrating the resilience of the IDI model in a volatile market environment, as was the case in the midst of the COVID-19 pandemic, is the performance shown in 2020, posting a 6.11% NAV growth rate. This was mainly led by improved fair values of the Private Equity Europe assets (+€36m) and liquid assets (+€12m), with the former benefiting from improved operational performance and higher valuation multiples at the end of the year, as well as the capital gains on the exit of HEA Expertise under very favourable valuation conditions agreed before the sanitary crisis, securing a solid 35% IRR. Even after having invested €32m over the course of 2020, IDI closed the year with a €124m-strong total liquidity position (€142m in FY19).

2022 and 2023: thriving and transformative years

After a resilient 2020 amid adverse market conditions, and a dynamic 2021 with 16 transactions totalling over €300m (+28% NAV growth), IDI delivered another solid performance in 2022 (+12% NAV, 15 deals) which proved to be a landmark year for IDI, as the Group embarked on a bold expansion into third-party asset management. This pivotal decision was marked by the acquisition of Omnes and the establishment of IdiCo, a newly-created entity merging Omnes’ private equity and private debt operations. Through this transformative step, IDI successfully doubled the scale of its third-party asset management business, reaching €1.5bn of AUM. This strategic shift toward a hybrid model—balancing proprietary investments (€25m-€60m, up to €100m in co-investments targeting French and European SMEs) with IdiCo’s smaller, focused investments (€5m-€25m in France) not only expanded IDI’s market reach but also diversified its revenue streams.

2023 was on a par with the previous years, with an 11% increase in NAV and, above all, a record 21 transactions. The Group’s stand-out deal was the sale of Flex Composite Group to Michelin for an enterprise value of €700m, yielding a 12x return on its initial investment and an IRR of 38%. This transaction significantly boosted IDI’s investment capacity, leaving it with over €300m in available funds.

In essence, whether in tranquil or more dynamic years, IDI enjoys the distinct advantage of choice. While 2024 has proved quieter, this is only a temporary lull, as the past two years alone have seen an impressive 36 deals. This serves to reaffirm the profound strength of IDI’s business model: not being constrained by time when the environment does not lend itself to investment.

IDI: a hands-on shareholder

In the holding company universe, one can distinguish three different types of management styles of the portfolio: first, there are those that keep their investments at arms-length and are content with collecting periodic dividends, secondly are those that get “down and dirty”, getting directly involved in the operations of their investee companies, which can quickly get complicated when new investments fall in completely different sectors.

Then, there is a third path, to which IDI ascribes to, a hands-on approach as a shareholder, as it is working in close relationship with the investee company’s management and getting involved in the supervisory board, but leaving the day-to-day operations to skilled managers who have the valuable knowledge in the respective sectors of activity. This avoids spreading the HoldCo’s resources too thin, which increases the likelihood of execution risks.

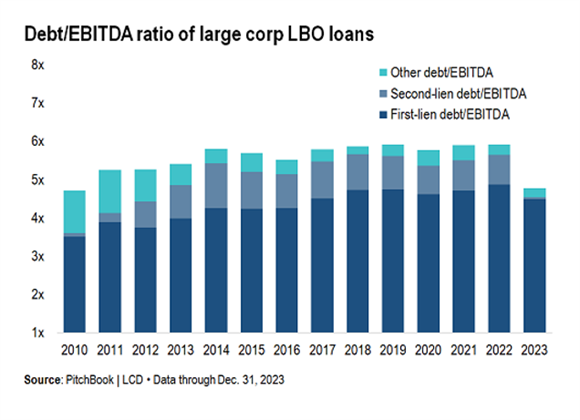

Regarding investment strategies, IDI specialises in LBO investments as well as growth capital investments in SMEs. The company’s judicious investment approach extends to the near-zero leverage maintained at the holding company level, with a relatively low average leverage ratio. Over recent years, IDI’s leverage ratio has oscillated between 2.5x and 3x EBITDA. While the 2023 figure was higher at 4x, it remains below the market norms (6x in 2022, 4.8x in 2023).

Source: PitchBook

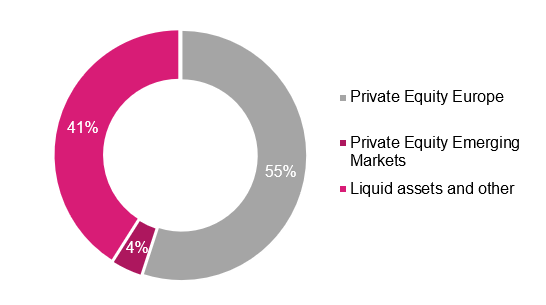

In terms of geographical breakdown, the lion’s share of the portfolio is Europe-based (France in particular), accounting for 45% of the NAV, with the emerging market exposure (4% of the NAV) being run through a third-party capital management model (combined with own equity capital investing) under the IDI Emerging Markets Partners umbrella. The remaining 51% is made up of IDI’s liquid assets, stemming from the sale of Flex Composite Group. This transaction considerably strengthened IDI’s financial position, giving it substantial investment capacity moving forward.

NAV breakdown as of December 2023

Source: IDI Annual report, AlphaValue

Concerning the size of the investments, IDI being a relatively smaller player in the private equity space, these range between €10 and €50m and can extend up to €150m with family office type co-investors, i.e. not time constrained as well. IDI is flexible in regards to the shareholding size, as its current portfolio includes majority, co-controlled and minority investments, usually determined by the scope of the deal.

An attractive high-growth portfolio

The portfolio is composed of 14 holdings, allocated across a variety of sectors, including many companies present in digitally-native businesses (reminding us of a smaller Kinnevik), which are supported by strong underlying trends with high-growth potential such as media streaming (Dubbing Bros), e-commerce (Group Positive), the energy transition (TucoEnergie) and social issues like education (Talis) and healthcare (Winncare Group).

Regarding the more industrial-type businesses, IDI previously held investments like Flex Composite Group, which followed a solution-based approach that brought added value and recurring revenue generation, setting it apart from its more commoditized, and hence cyclical, peers. While Flex Composite Group was sold in 2023, IDI’s diversified asset base continues to offer stakeholders exposure to unlisted, high-potential SMEs that may fall under the radar of equity investors.