A fintech with a banking licence

Swissquote Group Holding (Swissquote) is Switzerland’s leading online bank and one of the most renowned investment platforms. It mainly covers private clients but it also has a non-negligible B2B business. Institutional clients (such as asset managers) are indeed also using its trading platform and the bank has been able to leverage this high-quality trading platform to develop at an international level (through either partnerships or white labels).

As mentioned on Swissquote’s website (section “About us”), “Swissquote is not a typical Swiss bank”. According to our understanding, it is indeed more about financial innovation than traditional banking. This is the reason why we have classified the bank as a Fintech (Internet Banking/Fintech).

A solid B2C business with B2B as the new growth engine

The B2C side makes up the bulk of Swissquote’s net banking income as it contributes about 90% to it.

However, the company has also managed to develop over time a B2B side which is composed of partnerships and white-labelling. In 2016, for instance, Swissquote and PostFinance signed a white-label agreement whereby the Swiss Fintech acts as the trading platform for PostFinance.

Swissquote’s B2B market is also about onboarding asset managers. While less important in Europe and Switzerland, these represent a high proportion of clients in the Middle-East (Dubai) and 100% of the customers in Swissquote-recently opened a subsidiary (2020) in Singapore.

A strong CET1 ratio offering flexibility

Having a banking licence, the company is regulated as a bank with all the constraints that come with it. Indeed, it has to maintain a certain level of capital (namely common equity tier 1). The Swiss regulator imposes an 11.2% minimum CET1 ratio. As management is targeting a 15% CET1 ratio, we use this number for calculating the company’s excess capital (or net cash in the balance sheet).

Swissquote’s CET1 ratio stands at about 23% (Q420), well ahead of the regulatory requirements offering flexibility especially in terms of external growth or capital distribution. For the years to come, we use a growth in RWA in line with that of the revenues and a 30% payout ratio (with a minimum of CHF1) which would lead to a CET1 ratio in the area of 30% in 2024. This highlights the different investment case compared with traditional banks, because Swissquote, as an innovative financial institution, is more geared towards investments and technology and much less (if not all) towards an extensive use of its balance sheet.

Guidance 2021 – 2024

Management reached its 2022 guidance two years ahead in 2020. The COVID-19 pandemic, leading to a high degree of volatility together with stay-at-home orders, led to a sharp rise in the opening of new accounts and retail trading. The institutionalisation of crypto-currencies trading at the end of 2020 also helped Swissquote which had already developed a strong franchise in that asset class.

2020 was therefore both an exceptional year for the Swiss Fintech as well as a game-changer going into 2021 and the future.

Hence, management is targeting another year of strong growth in 2021 with revenues expected to be up +15%. Pre-tax profit should rise +23% at the same time.

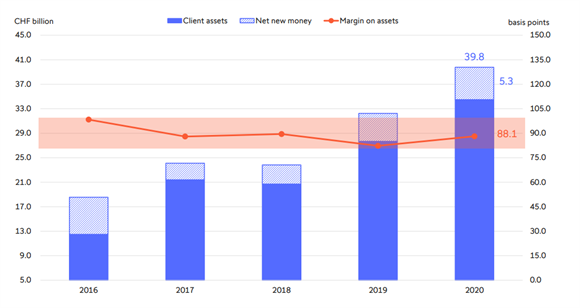

Adjusted for credit losses in trading income in 2020, it would reach 8% growth in revenues. This will be possible through the democratisation of the trading of crypto-currencies. At the same time, the opening of new accounts will remain buoyant and management expects net new money of CHF5bn.

The long-term target (2024) is bullish as well and well detailed by management, which makes it highly achievable.

Management expects revenues at CHF500m in 2024, which represents a 12% CAGR and a CHF200m pre tax profit (twice the 2020 level and four times the 2019 level).

Reaching this level of revenues would be equal to attracting about CHF5bn net new money per year together with a 90bp margin on assets. This is achievable given the recent momentum.

The integration of Swissquote Europe bank (former InternaxX), the ongoing developments in the Middle Eastern and Asian (Singapore) markets should help reach the assets under custody target.

Swissquote indeed expects balanced net money inflows with half coming from Switzerland and the other half from “the rest of the world”.

All these numbers only refer to organic growth. With a comfortable level of capital and cash generation each year, the Swiss Fintech will be in position to grow externally as well (cf the Money Making section).

Competition

Swissquote has to face the competition of other brokers, like SaxoBank (CornerBank) or IG Group and other low-cost brokers.

Traditional banks such as UBS and Credit Suisse are also obvious competitors for Swissquote in Switzerland. However, trading costs on their platforms turn out to be more expensive.

Through R&D, the Swiss Fintech has positioned itself at the junction of these offerings. It indeed offers the combination of the reliable “Swiss quality” with a friendly interface at an affordable price. Swissquote’s trading platform indeed proposes a wide range of asset classes (equities, bonds, OTC products, crypto-currencies) on a global scale (US, European and Asian assets).

Positioning itself as a quality broker enables Swissquote to be less dependent on pricing and more on the depth of its investment solutions offering (in both asset classes and geographic terms). The average client balance (CHF100,000) is indeed higher at Swissquote than at other online brokers. Hence, the Swiss Fintech has managed not to be hurt by these competitors (which are also not so profitable).

The chaos in the markets at the beginning of 2021, with the corner around Gamestop in the forefront, has questioned the reality behind the free fees/commission offered by some platforms like Robinhood. This commission-free trading has indeed a liquidity price in the end and should, from now on, ring a bell for retail investors.

Robinhood’s and other commission-free brokers would find it hard besides to impose their business model in Europe. On top, the level of interest rates (negative) and the regulatory framework with MIFID2 at the forefront require the concept of best execution, disclosures of any inducements, etc.